August 8, 2017

Aframax demand in the Caribs could be collateral damage to further sanctions

On July 31, the United States government announced economic sanctions on President Nicolas Maduro in response to recent Venezuelan election results that are largely viewed as illegitimate and a move towards a dictatorship regime within the nation. The sanctions are an embargo on all US individuals and organizations doing business with President Maduro. Although no formal oil-related sanctions have been included in the sanctions as yet, there is speculation that sanctions on the oil industry may follow. Venezuela holds the world’s largest oil reserves.

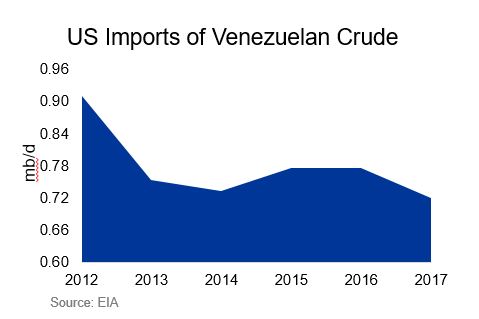

At it’s height in the late 1990s, the US imported ~1.4 mb/d from Venezuela – more than their imports from Mexico, Saudi Arabia, and Canada. However, by 2016, those imports halved to ~0.7 mb/d, falling a distant third behind Canada and Saudi Arabia. Should an oil embargo be enacted, US refiners will be forced to source crude further afield, which will ultimately be a hit on their margins.

|  |

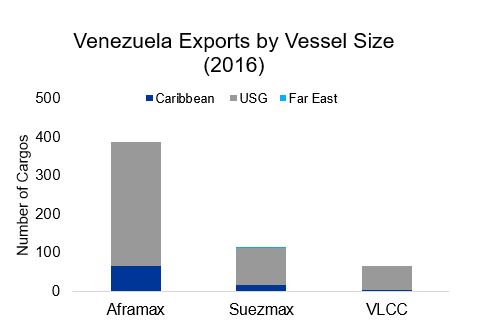

The lion’s share of Venezuelan exports to the US move on Aframax tankers, as shown on the chart above. Our data suggests 323 movements from Venezuela into the USG in 2016. The obvious outcome of a Venezuelan oil embargo would include a serious decline in Aframax demand in the Caribs market.

While Aframax movements out of Venezuela to the USG would likely evaporate under US sanctions, there could be some upside from a more volatile trading pattern. Longer haul movements from WAF and the MEG into the USG, as well as an uptick in lightering demand, could provide some upside to tanker demand. In addition, volumes that would have previously moved to the US will likely move to Asia on VLCCs, which would further stretch the VLCC fleet between the MEG and the Atlantic. Such trading volatility could provide some upside to rates through an otherwise down time in the market cycle.